Why are you removing indexation from DB schemes?

To help employers manage the high costs and risks associated with a DB scheme. However it should be noted that employers will have the discretion to provide indexation if they so choose; many already provide more indexation than the statutory minimum.

We are removing the statutory requirement to index pensions in payment for future accruals of benefit only from the date of any legislative change– benefits already accrued will not be affected.

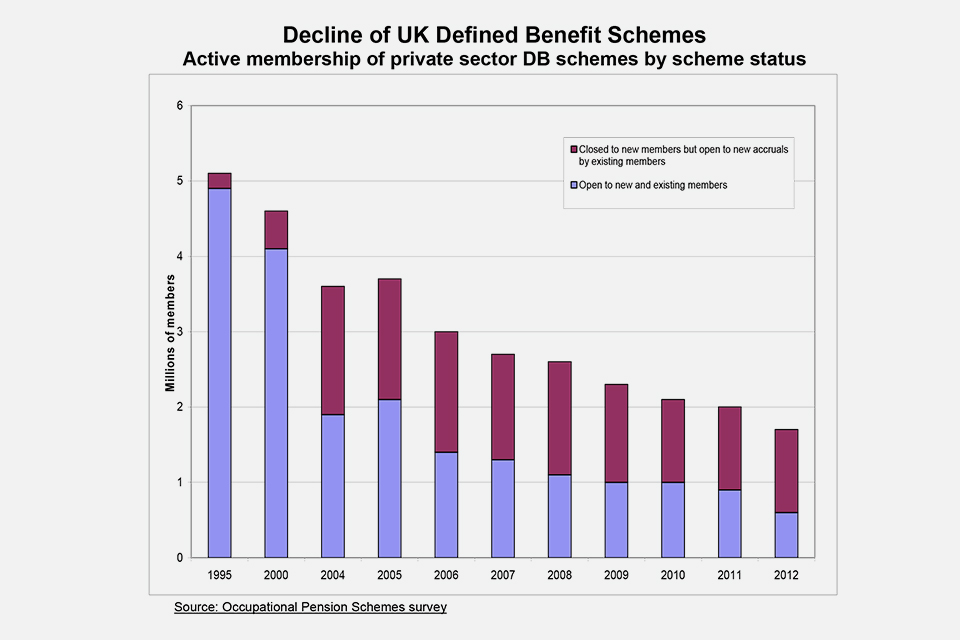

Defined Benefit schemes have declined rapidly in recent years and unless we act there are going to be very few open DB schemes left by the next decade. Deregulating DB pensions will mean that employers will be able to offer more flexible schemes that, whilst they may be less generous compared to traditional final salary DB pensions, should offer members more (in terms of pension outcome and certainty), than they would get if the only alternative for employers are the current DC arrangements where the member bears all the risks. Inflation protection is a costly provision that we believe employers should have a choice over whether or not to offer their members.

We are consulting on the idea of removing the statutory requirement to index pensions in payment for future accruals of benefit only – benefits already accrued as well as revaluation of benefits for deferred pensions will not be affected. Employers will also have the discretion to provide indexation for future accruals of pension benefit if they so choose; many already provide more indexation than the statutory minimum. The key point is that it should be left to employers to decide the shape of benefits – not Government.

The Government is currently legislating in the Pensions Bill to replace the current two-tier state pension system with a single-tier state pension. Like the current basic State Pension, the new pension will be up rated annually by at least the growth in earnings (over the longer term, earnings growth tends to be greater than increases in prices). This will therefore provide individuals with a source of retirement income that is protected against inflation. Where individuals have other financial assets (including additional DC pensions), these may also yield income streams that provide protection against inflation.

Sam

DA Team

DWP